日本クレラス税理士法人の中川好隆が、遺族年金について解説。遺族年金は、被保険者が死亡した際に家族が受け取る年金で、遺族基礎年金と遺族厚生年金の2種類がある。配偶者は特定の条件下で終身受給可能。遺族基礎年金は基本額と子供の加算額で計算し、遺族厚生年金は故人の老齢年金の報酬比例部分の4分の3となる。受給できない場合は寡婦年金や死亡一時金が支給される。中程度の企業と個人を対象に事業承継や相続に関するアドバイスを提供。

When thinking about pensions, many people think of the old-age pension as a source of funds for retirement. However, there is also a survivor’s pension that is paid to the family left behind when the breadwinner passes away.

In this article, Yoshitaka Nakagawa from Nihon Cleras Certified Public Tax Accountants shares his knowledge and experience accumulated over years of working as a tax accountant to explain survivor’s pensions.

This article will specifically focus on the case where a husband passes away and the wife is eligible to receive a pension.

Table of Contents:

What is a survivor’s pension?

How long can a spouse receive a survivor’s pension?

How is the amount of survivor’s pension for a spouse calculated?

What to do if you can’t receive a survivor’s pension?

Conclusion

What is a survivor’s pension?

A survivor’s pension is an insurance benefit that a dependent survivor can receive when the insured person covered under the National Pension or Employees’ Pension Insurance dies.

There are two types of survivor’s pensions: “Survivor Basic Pension” and “Survivor Employee’s Insurance Pension.” A wife whose husband was covered under the National Pension can receive the Survivor Basic Pension if the husband meets the eligibility requirements.

In addition, individuals covered under the Employees’ Pension Insurance can also receive the Survivor Employee’s Insurance Pension if they meet the eligibility criteria.

How long can a spouse receive a survivor’s pension?

Let’s explain how long a spouse can receive the “Survivor Basic Pension” and “Survivor Employee’s Insurance Pension.”

Survivor Basic Pension

This benefit can be received until the end of March in the year when the child reaches 18 years old or until the child reaches 20 years old if they have a Class 1 or Class 2 disability. Once the child reaches adulthood and this period is over, the payment period for the Survivor Basic Pension ends. However, if the spouse remarries while there are children, the spouse will no longer be eligible for the Survivor Basic Pension.

Survivor Employee’s Insurance Pension

If there are children when the husband passes away or if the wife is over 30 years old, the spouse can receive this pension for life starting from the month after the husband’s death. On the other hand, if there are no children when the husband passes away, or if the wife is under 30 years old, the payment period is only 5 years from the month after the death.

How is the amount of survivor’s pension for a spouse calculated?

Now, let’s take a look at the actual amount of survivor’s pension that a spouse can receive.

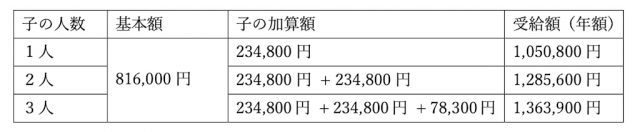

1: Survivor Basic Pension Amount (as of April 2020)

The Survivor Basic Pension amount is calculated by adding the child allowance to the basic amount. The child allowance varies depending on the number of children, with children being defined as those who have not reached the end of the year when they turn 18 (March 31) or those who are under 20 years old. Those with a Class 1 or Class 2 disability are also included.

Below are the basic amount and child allowance:

Basic Amount:

- For those born after April 2, 1955: ¥816,000

- For those born before April 1, 1955: ¥813,700

Child Allowance per Child:

- For the first and second child: ¥234,800 each

- For the third child and beyond: ¥78,300 each

The table below summarizes the annual payment amounts for wives with 1-3 children born after April 2, 1955.

Wives without children or with children aged over 18 (20 in case of Class 1 or Class 2 disability) cannot receive the Survivor Basic Pension, so please be aware of this.

2: Survivor Employee’s Insurance Pension Amount

The survivor’s pension that a survivor can receive is 4/3 of the proportionate part of the deceased person’s old-age pension. The proportional part is determined based on the period of pension coverage and past earnings. The calculation method is as follows:

Calculate: (1) (average standard monthly salary ※1 × 7.125/1000 ※3 × months of membership before March 2003 + average standard salary ※2 × 5.481/1000 ※3 × months of membership after April 2003)

Calculate: (2) (average standard monthly salary ※1 × 7.5/1,000 ※3 × months of insured period before March 2003 + average standard salary ※2 × 5,769/1,000 ※3 × months of insured period after April 2003) × 1,041 ※4

The larger amount between (1) and (2) is considered the proportional earnings part.

※1 Average Standard Monthly Salary = Total standard salary amounts for each month during the period of insurance before March 2003 divided by the total period of insurance before March 2003.

※2 Average Standard Monthly Salary = Total standard salary amounts plus standard bonuses for each month during the period of insurance after April 2003 divided by the total period of insurance after April 2003.

※3 [For those born before April 1, 1945, the benefit ratio is different.

※4 For those born before April 1, 1939, the number is 1,043.

When calculating the proportionate earnings part, if the period of insurance coverage for the Employees’ Pension is less than 300 months (25 years), it is calculated as 300 months.

If a person over the age of 65 who is entitled to receive an old-age pension due to their own contributions receives a survivor’s pension equivalent to 4/3 of the deceased person’s old-age pension. The amount the survivor pays is determined by comparing the “proportional part of the deceased’s old-age pension” and “half of the proportional part of the deceased’s old-age pension plus half of the surviving spouse’s old-age pension” to the higher amount. This is the amount of the survivor’s living pension.

Additionally, in the case of a husband’s death when the wife is between 40 and under 65 years old and there are no children living together or children under 18 years old (or children who have reached adulthood), the wife is eligible for an additional ¥612,000 (annually) for the Survivor Employee’s Insurance Pension.

What to do if you can’t receive a survivor’s pension?

If the wife becomes independent of children or doesn’t have any children, she may not be able to receive a survivor’s pension. However, she may be eligible for the Widow’s Pension or a one-time death benefit.

1: Widow’s Pension

If the husband, who was exempt from paying National Pension contributions for 10 years until the month before the month of death, and had paid National Pension contributions for more than 10 years, dies, then a widow who was supported by him for at least 10 years and hasn’t reached 60 years old will receive the benefit. The amount of the Widow’s Pension is 4/3 of the Old-Age Basic Pension calculated only during the husband’s first insured period.

2: Immediate Death Benefits

If a person paying insurance contributions for 36 months or more as a first insured person until the month before the month of death, without receiving the Old-Age Basic Pension or Disability Basic Pension, dies, immediate death benefits of ¥120,000 to ¥320,000 are paid depending on the number of months of contribution, to surviving dependents who depend on the deceased’s livelihood.

In addition to “Widow’s Pension” and “Immediate Death Benefits,” in cases where a husband’s death is recognized as an occupational accident (work injury), compensation may also be received under the Workers’ Accident Compensation Insurance.

Conclusion

In this article, we introduced the mechanism and amounts of survivor’s pensions available to wives after the husband’s passing. Survivor’s pensions are divided into “Survivor Basic Pension” and “Survivor Employee’s Insurance Pension.” However, the eligibility period and amounts vary, so it’s recommended to check how much survivor’s pension you are entitled to receive.

● Interviewed by / Yoshitaka Nakagawa

Representative Director and Tax Accountant at Nihon Kleras Certified Public Tax Accountants

With extensive experience in tax consulting for companies listed on the Tokyo Stock Exchange First Section, tax return support, organizational restructuring consulting, business succession consulting, accounting outsourcing, and early closing services. Our office provides advice on “smooth business succession” and “inheritances without disputes” tailored to the circumstances of each client and has earned high praise and trust from many clients.

Nihon Kleras Certified Public Tax Accountants (source)

{kind=link}

Composition and editing / Keiko Matsuda (Kyoto Media Line /